Beautiful Clean Coal

4 Stocks set to benefit from the World's most hated Supercycle...

Introduction

Coal is one of the most hated commodities today - the advent of “ESG” meant that coal mining became THE go-to industry to vilify, the poster child of global warming and main driver of carbon emissions. In the process of scoring easy political victories over the recent decade, the world came to forget that the 2 main types of coal are indispensable in the continued growth of mankind. Thermal coal is burnt to provide cheap, reliable baseload power that keeps our lights on - and continues to alleviate millions out of poverty because it is what developing/emerging economies can afford as they continue industrialising. Metallurgical or steel-making coal, is burnt in blast furnaces to produce steel - the very input that enables our infrastructural boom, “green transition”, AI buildout, and increasingly so - wartime economies.

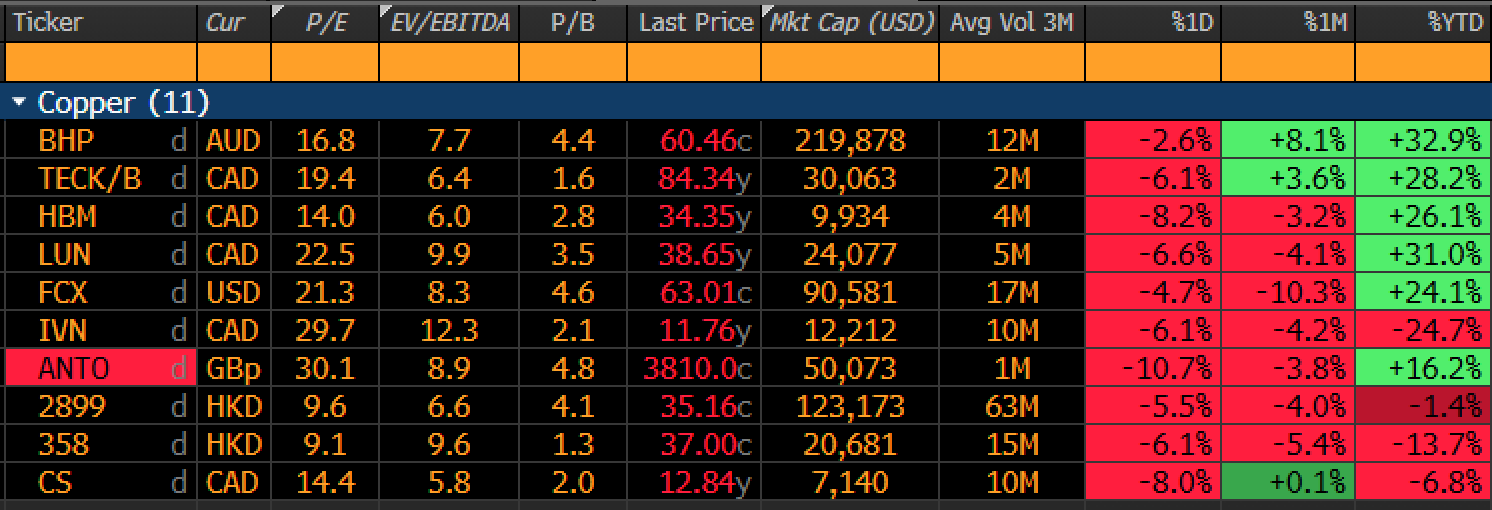

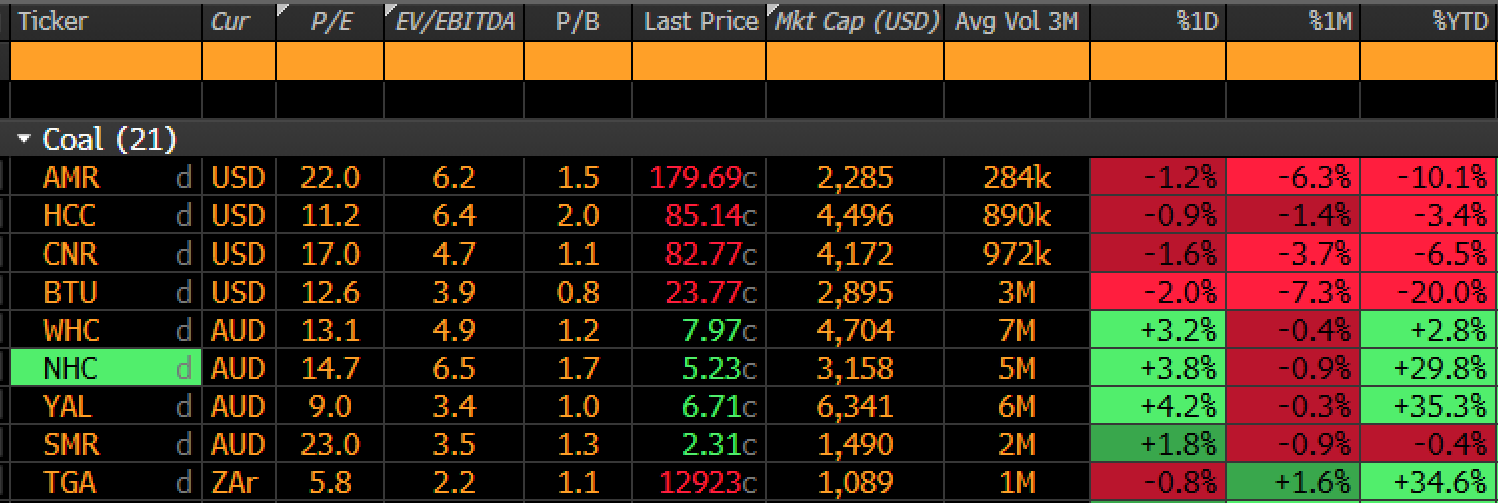

The focus of this piece will be on thermal coal given the confluence of near-term macro catalysts on top of the long term scarcity story. But if you were to ask me if I thought thermal and/or met coal will be victims of structural demand decline by 2040, I would be taking the other side of that bet all day long. To underscore how hated coal remains, we just have to look at the valuation multiples the copper peer group trades at vs coal companies in relation to where commodity prices already are vs their respective cost curves. Today, copper producers trade at >8-10x EV/EBITDA on $6/lbs copper (prices that are +30-40% ABOVE the 90th percentile of the cost curve) vs coal producers trading at <5-6x EV/EBITDA on $140-150/ton Newcastle Thermal Coal or $220-240/ton PLV HCC Met Coal (prices BELOW 90th percentile cost curve)

There is a clear relative valuation arbitrage here: why should coal trade at 5x EBITDA on bottom cycle earnings and copper at 8-12x EBITDA on upcycle earnings, when I have little doubt that we will all be using (more of) coal and copper come 2040?

What we are buying here are low cost, long-duration assets whose scarcity value will only increase with time, whilst the market still thinks that coal will be phased out in 5 years on “castle in the air” physics.

It is as if green steel will sprout out of nowhere to replace the 90% share of blast furnaces in operation AND many under construction, while a mixture of unstable wind, daytime solar and expensive/long-lead time nuclear will replace the grids of the world’s largest developing economies overnight.

I believe the whole ESG indoctrination is the biggest policy mistake the developed west has made that has serious implications for their future economic potential. Electricity is the biggest limiting factor in the AI revolution, and only China understands that solving for energy abundance/having the lowest cost energy molecule is the foundational competitive edge for scaling AI applications. If you search out objective journalism, it seems like some in the West are beginning to realise just how backward and unprepared the US grid is for the AI revolution vis-a-vis China.

Consistent with my investment framework, I always try to identify a confluence in macro and micro for high probability set-ups, and thermal coal (and to a lesser extent, metallurgical coal) are at the cusp of inflection today:

Macro: The onset of the Iran War and the destruction of major liquified natural gas (LNG) production plants in the gulf marked a significant turning point for energy markets. While stranded oil exports and onshore storage would likely ease with a lag if/when the Strait of Hormuz is open/definitive end to the war is reached, gas plants that are out of commission will take years to repair at the minimum. With regional gas prices in Asia and Europe doubling since the war started, thermal coal switching in combined cycle gas plants is the only go-to solution that is now exceedingly economic and reliable, to keep the lights on

Micro: All 4 of the coal producers we are profiling have conservative balance sheets, with different degrees of leverage to higher coal prices. Naturally, the 2 smaller producers we are profiling would have the highest torque to a sustained thermal coal upcycle, while the 2 larger hybrid coal producers are what we deem ‘best in-breed’ long term holdings, given their low-cost, long duration asset base with great management teams that have a history of distributing significant cash to shareholders

Keep reading with a 7-day free trial

Subscribe to Apeconomics to keep reading this post and get 7 days of free access to the full post archives.